Are you tracking the Market Recovery Monitor each week? Utilizing data and benchmarking to navigate recovery will be a key focus of the 2021 Hotel Data Conference. Click here for registration, with both in-person and virtual options available for our 13th annual event in Nashville.

Previous MRM versions: 19 June | 26 June

Week ending 3 July

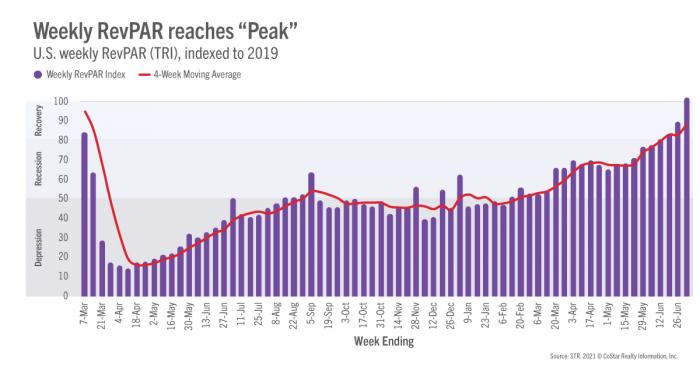

Prior to the pandemic, holiday weeks tended to be lackluster due to the lack of business and group travel. During the pandemic era, that trend seems to be returning. Week over week, demand fell 1.7 million room nights, but the decline was less than what was seen in the comparable week of 2019 when demand fell 3.7 million room nights. There is limited business and group demand now, so the leisure surge mitigated the loss as more rooms were sold this week (25.1 million) than in the comparable 2019 week (24.8 million). For the week ending 3 July 2021, occupancy was 65.4%, down 4.4 points from the previous week. Daily occupancy ranged from 60% on Sunday, 27 June 2021 to 76% on Saturday, 3 July 2021. All days posted week-to-week declines in occupancy, except for Sunday, which was up by its largest amount of the past four weeks. On a total-room-inventory basis (TRI), which accounts for temporarily closed hotels, weekly occupancy was 62.8%.

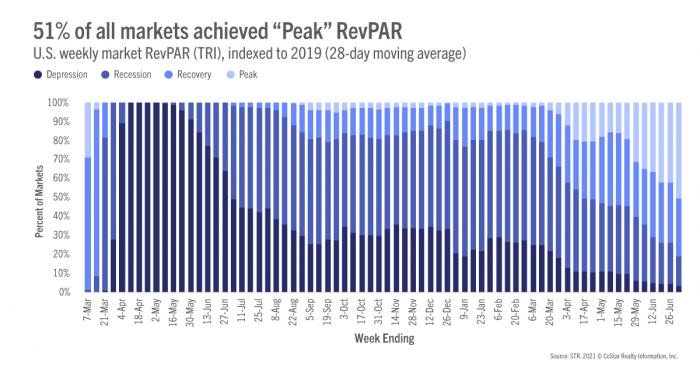

With stronger holiday demand in the week than what was seen previously, it’s no surprise that 69% of all markets saw demand indexed to 2019 above 100 with more than a third of all markets having a 10 percent demand premium over their 2019 results. However, on a week-over-week basis, nearly every market saw weekly demand decrease except for eight, led by Denver and Seattle. The latter was driven in part by the record-breaking heat wave that affected the Pacific Northwest. Despite lower weekly demand, 66% of all U.S. hotels had occupancy above 60%, down from 75% a week ago. History tells us that we can expect demand and the percentage of hotels with occupancy above 60% to rebound in the week ending 10 July 2021.

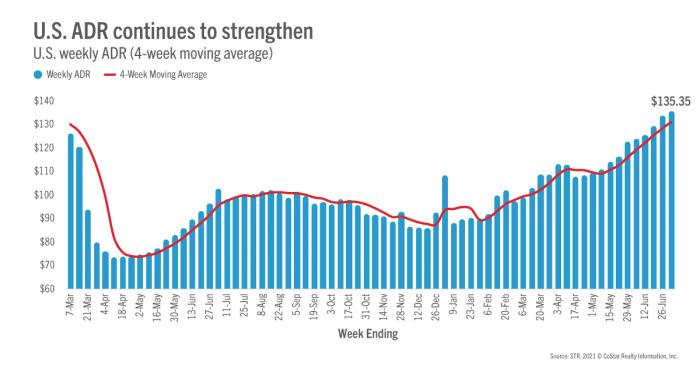

While the week-on-week decline in demand and occupancy—which was still good on a relative basis—caught our attention, the more positive news from the week was ADR, which increased to US$135. That was the highest weekly level since the first week of 2020 that included the New Year’s holiday. In fact, this week’s ADR was the seventh highest for any of the past 130 weeks. On an inflation-adjusted basis, ADR was also at its best since the beginning of 2020. Excluding the Top 25 Markets, ADR is the highest it has ever been. While Top 25 Market ADR is not at a record high, it was at its highest level since March 2020.